Why I Sold Out of PETS After Only a Month

Grading Q2 25 - The Good, The Bad, and Expectations for H2 25.

After Q2 25 earnings and a recent Sidoti Conference presentation, I exited my PETS position. It was never my intention to profile a stock and then a month later post saying I’ve sold out. But I did, so here’s my rationale why.

The Good

Gross margin increased sequentially from 26.4% to 29% and quarter-over-quarter from 28.2%.

Balance sheet - inventory decreased massively to $13.1 million in the most recent quarter from $28.6 million as of 3/31/24. The inventory reduction was due to an intentional SKU rationalization. I believe there was a large push in Q2 because at the end of Q1 25, inventories were $25.5 million. This has some negative nuance. The business historically has carried ~$20 million in inventory - what happens when inventory needs to be replaced?

Average order value inched up to $96 from $94. This was largely driven by general inflation in MAP pricing - not actually through larger order sizes. Again, some negative nuance even in the positives.

No need for capital - $52 million in cash and no debt.

The Bad

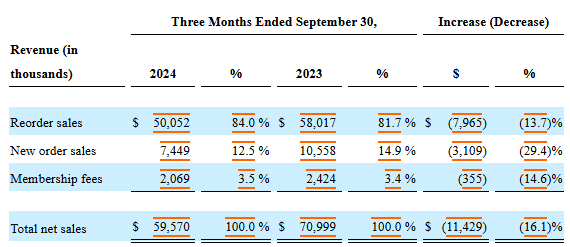

Two consecutive quarters of revenue decline. This comes at a time where management has been intentional about their focusing on retention of customers before turning on the growth engine. Q1 revenue comped at -13.2% and Q2 at -16.1%. Not only are the comps negative, they are trending in the wrong direction. Management has talked about retention, but the numbers in Reorder Sales from Q1 25 to Q2 25 show a worrisome trend for retention as reorder sales decreased almost $10 million sequentially.

Although gross margin increased, gross profit dollars were down sequentially from $17.9 million to $17.3 million.

Customer acquisition is trending down - 77,000 new customers in Q2 25 vs. 113,000 in Q2 24. 197,000 new customers in H1 25 vs. 250,000 new customers in H1 24.

Customer acquisition costs were $60 in Q2 25 vs. $49 in Q2 24. Putting this point and the former point together, not only is the business welcoming fewer new customers, they are doing it less cost effectively than before.

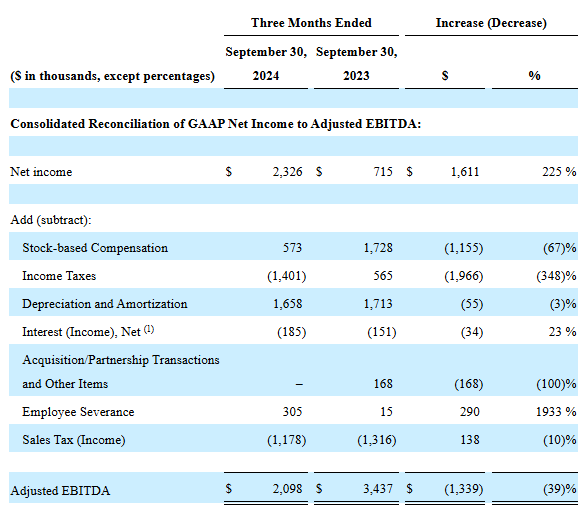

Adjusted EBITDA of $2.1 million. Many investors have correctly pointed out that the net income of $2.3 million in the quarter was largely due to a $1.4 million income tax benefit. Initially, I was cautiously optimistic because the D&A addition of $1.6 million back to Adjusted EBITDA “corrected” for the income tax benefit. However, this left the Adjusted EBITDA margin at 3.5%. This 3.5% is after the company has said they’ve taken out most of the duplicated costs, focused on retaining customers, and now are moving forward with spending to acquire new customers.

Q3 and Q4 - A Big Deterioration of Margins?

Earlier this month I did some price comparison shopping looking to purchase Heartgard, Nexgard, and pill pockets for my dog. For those that don’t have pets, the first two are common monthly medications given to dogs for heartworm/other worms (Heartgard) and flea/tick prevention (Nexgard). In my earlier write-up, I mentioned that PETS and competitors adhere to MAP pricing. The way companies differentiate themselves within the industry is through promotions, service, convenience, or some combination of all three. Looking at the exact same bundle of those three items, the price from PETS for my dog was just under $100 vs. $141 through Chewy. This was through applying the most prominent discount displayed on each website and opting in to the auto-ship option. As a consumer this was great. As an investor, this leads me to believe that the company is entering into a period of heavy discounting to acquire customers. This aligns with messaging the CEO has provided in earnings calls and recent Sidoti presentation.

I’m seeing the possibility of the next couple quarters from PETS showing: 1) diminishing gross margins from discounting, 2) increased customer acquisition cost from marketing spend, 3) 1 & 2 leading to net losses in the quarters, and 4) revenue continuing to diminish based upon trends and lack of differentiation in the space. Even if revenue increases, at what cost? It is entirely possible the business is stuck in the doomed tradeoff - be profitable and shrink top line vs. grow top line but be unprofitable.

Conclusion

I am still rooting for the management to turn the business around and plan to keep following the company’s progress. However, I took advantage of the market’s irrational response to a bad quarter and exited. The market has priced in progress that has not actually happened, and I’m less optimistic about the potential turnaround moving forward.

Disclosure: No position.

Thanks for the update .

Could I ask ?

How many stocks do you now currently own and do you still rate Crexendo ?

Cheers