PetMed Express, Inc. (PETS)

In the early innings of a turnaround.

Price: $3.90

Market Cap: $80.3 million

Shares Outstanding: 20,600,652

FY End: March 31 (currently in FY 2025)

Executive Summary

PetMed Express, Inc. (NASDAQ: PETS) has already lived a full life as a company. They have been a growth story, a dividend company, and most recently, an unmitigated disaster. However, with a new management team in place, things are quickly changing and I think the company has one last act as a turnaround story. The fundamental business has remained unchanged for nearly 30 years and is extremely cash generative when run well. The new management team is focused on returning to the core business that made PETS successful for 25 years. Within 2 months, the new CEO returned the company to GAAP profitability in the most recent quarter giving signs the turnaround is already underway.

Company History/Business Overview

PetMed Express is a pet wellness company that sells prescription medications, supplements, prescription food, non-prescription food, and pet supplies for dogs, cats, and horses.

PetMed Express was founded by Marc Puleo and Yali Golan as an alternative solution to veterinarians charging high prices for medications. By the fall of 1997, the company launched their first catalog and began advertising on TV as 1-800-PETMEDS. Sales were driven through the catalog, postcards, customer service representatives, and the Internet. By Q1 2005, more than half the sales were Internet based. The stock was traded on the OTC Bulletin Board from 1997 until 2000 when the company up-listed to the NASDAQ. However, the real story starts in 2001 when Menderes Akdag joined as CEO and Bruce Rosenbloom as CFO.

Akdag’s Tenure (2001-2021)

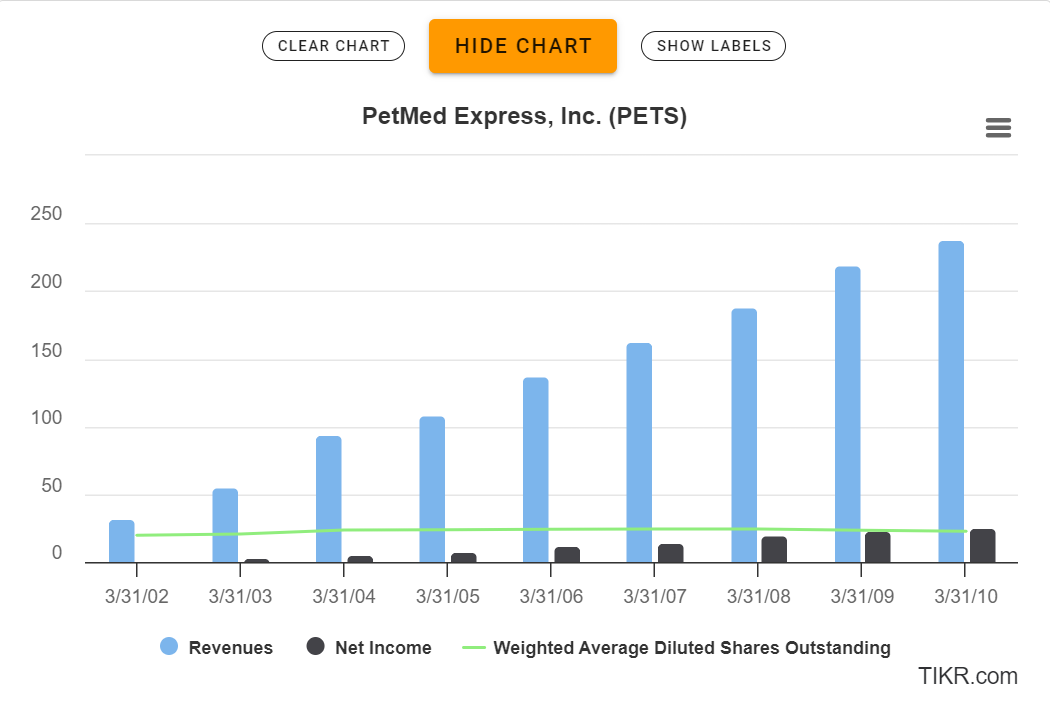

Under Akdag and Rosenbloom, the company had a run of 10 years from 2001-2010 that is every investor’s dream: revenues, gross profit, operating income, net income, and EPS all grew while shares outstanding remained relatively flat. The company went from a GAAP loss in 2001 to growing EPS consistently every year. The execution was strong and the business was added to the Russell in 2004. In 2006, the company announced the first of three $20 million share repurchase programs. The repurchases were never significant, but helped to keep shares outstanding steady and offset any material dilution.

In FY 2010, PETS hit a bit of a holding pattern. Consumers were more price sensitive, new large retailers started entering the space, and vets started pricing more competitively. PETS increased advertising spending to maintain customers. During this period, gross margins dropped from the low 40s to the mid-to-low 30s. Analysts on conference call transcripts were clearly getting frustrated as sales were stagnating and the company was sitting on $50-$60 million in cash. In August 2009, PETS announced their first quarterly dividend of $0.10 per share. The company raised the dividend periodically ending at $0.30 per share. In December 2012, the company issued a $1.00 per share special dividend. The company transitioned from a growth story to a capital return to shareholders story.

By 2016, the company started shifting away from advertising through TV to more targeted Internet-based advertising. This helped the company break free from a perennial trap that plagued them as advertising costs surged during election seasons. Now targeted ads were more effective and there was less competition for advertising space. Sales picked up again, reaching the new, stabilized base of $270-$280 million per year in revenue. I would argue this new base was driven through three factors: 1) targeted internet advertising, 2) a sustained increase in advertising spending, and 3) a growing TAM as the pet market has continued to expand. In September 2019, PETS introduced their loyalty program to get discounts on future orders. By December of 2020, it was shared that approximately 20% of customer orders had loyalty credits applied.

In 2021, the company announced they would not extend Akdag’s contract. From the company’s conference call in the interim period between CEOs, it was clear the Board of Directors was frustrated and felt like the company was losing momentum.

Hulett Era (2021-2024)

In August 2021, the company announced Mathew Hulett as CEO. He came to PETS from Rosetta Stone and had an objectively successful track record of working with and selling public companies.

In his first conference call with the company, he showed a picture of his dog on the slide deck. He shared that at 51 years old, this was his family’s first dog and he had no idea what they were getting into - foreshadowing his tenure with the company. On that same call, Hulett was already talking about ways to expand the company beyond pet medicine.

Huletts tenure could be defined by three things:

Launching of AutoShip and Save in 2021. This was the only successful thing from his tenure. Now, over 50% of revenue comes from AutoShip and Save which gives consumers convenience and gives PETS a nice solid base of recurring revenue.

Vetster Partnership - in April 2022, the company participated in the Series B round for Vetster and gave PETS an entrance into the pet telehealth space. This gave consumers 24/7 access to over 70,000 veterinarians.

PetCareRX - In April 2023, the company closed on its acquisition of PetCareRX for $36 million in cash. PetCareRX had approximately $40 million in annual revenue and 200,000 customers. The two companies were substantially similar with one caveat that PetCareRX also sells food.

With Hulett’s spending, hiring of his own executive team, and focus on shiny new objects instead of the profitable core business, the company began losing money for the first time since becoming a public company. By October 2023, the company had to suspend their quarterly dividend. The cash balance of over $100 million Hulett inherited in 2021 shrank to around $50 million by his departure in April 2024. The long-time CFO, Bruce Rosenbloom resigned. It was clear from commentary in the conference calls, Hulett did not have a grasp on the economics, the CFO was frustrated with him, and analysts were pointing out large discrepancies in the reality of the business vs. the CEO’s perceived reality. This exchange from the Q3 2023 conference call is a microcosm of Hulett’s tenuous grasp on the numbers:

Enter: Sandra Campos (April 2024-Present)

On April 29 this year, the Board separated from Hulett and appointed Sandra Campos as CEO. Campos previously joined the Board of Directors in May 2023. She is addressing the extremely low hanging fruit left behind from Hulett’s tenure. For example, PetCareRX was left to run as a completely separate business from PetMed Express. The businesses were not only running two separate ERPs, but they were even competing against each other in bidding for advertising slots!

In her first month, Campos focused on using marketing dollars for customer retention to better understand the company’s customer base and how to segment customers and personalize the experience to better engage customers. In September, this shifted to advertising being spent 60% on acquisition and 40% on retention.

The company is now re-focused on the enormous opportunity back in the core prescription business and thinking about logical add-ons like shampoos and topicals rather than acquisitions. Campos is talking about serving the needs of customers and leveraging their call center and 28 years of data to offer customers a seamless experience by having the right product at the right time at the right price.

In addition to focusing on customers, the business is addressing two large opportunities: AutoShip and private label prescriptions. AutoShip is currently 56% of the business and Campos believes this number can increase. The company has expanded options for AutoShip like skipping an order, changing the order frequency, and is currently evaluating having OTC products on AutoShip. Additionally, PETS is focusing on expanding their private label program. Currently, generics medications are less than 5% of the company’s business. Private label medicines have higher margins for the company and are cheaper for the customer. Unlike human generics medications, economic profits do not get fully competed away. The company is working with their veterinary advisory board to discuss what consumers are currently demanding, what works with animals, and what should not be explored. This advisory board of veterinary professionals meets to discuss what they are currently prescribing, chronic issues they see with patients, what is working well in their practice, and what customers can do from a preventative standpoint. The advisory board plus attention to the company’s 28 years worth of data is helping PETS to focus on how to drive value to customers and make decisions like what prescriptions to go after in the private label market.

Campos was CEO for only two months during the quarter ended June 30, 2024. Despite that, she was able to slash general and administrative expenses from $15.7 million in the June 30 2023 quarter to $4.9 million for the June 30 2024 quarter. Granted, $8.7 million of this was a reversal of stock compensation, but there were real savings as well: $0.2 million decrease in payroll expense, $0.2 million lower in professional fees, and importantly, $0.5 million in variable and other overhead expenses. Campos has been clear about addressing the low hanging fruit and cost issues in the business to return the company to profitability. It’s still early, but signs point to management following through on their plans.

Financials

PETS is a simple business that reports in one segment. At its core, they sell OTC supplements, prescriptions, and food for dogs, cats, and horses. Throughout the company’s life, conference calls and press releases have hinted that flea/tick/heartworm monthly medication have always been around 50% of revenue. There was previously a seasonality component to that, however, over time this has mitigated as northern climates do not freeze long enough during the winter and ticks live longer throughout the year. As of 2019, the company began sourcing 100% of products directly from manufacturers.

Revenues have been relatively stagnant since FY 2019 around $283 million per year. The business was a temporary Covid winner with sales rising to $303 million in FY 2021, but sales have since fallen back into the $280 million range. Over time, PETS’s gross margin has been competed away due to competition from existing players (vets) and new entrants being aggressive on price. Gross margin has slowly declined from around 41-42% prior to 2005 to the mid 30s. As vets became more price competitive and new players entered, they further declined. Now, gross margins have begun to stabilize around 27-28% over the last 5 years. Gross margin varies quarterly as PETS and other players will offer discounts when competition increases. The company’s average order size has grown from $73 in FY 2004 to $94 in FY 2024.

The two big operating expenses for the business are general & administrative and advertising. Historically these levers have been able to be pulled up/down to change results. Under Akdag, G&A historically was 8-9% of revenue and advertising was 7-8%. Under Hulett, advertising was relatively flat at 7-9% of revenue, but G&A as a percentage of revenue grew to 20% by FY 2024.

Inventory fluctuates due to the business being opportunistic in their inventory purchases. Inventory averages around $20 to $30 million based on the company’s purchases and availability. Generally, the company does not have problems sourcing inventory and the only minor issues are when food suppliers do not have as much inventory as the company would like to stock. Inventory turnover has averaged a healthy 7.5X over the last 10 years.

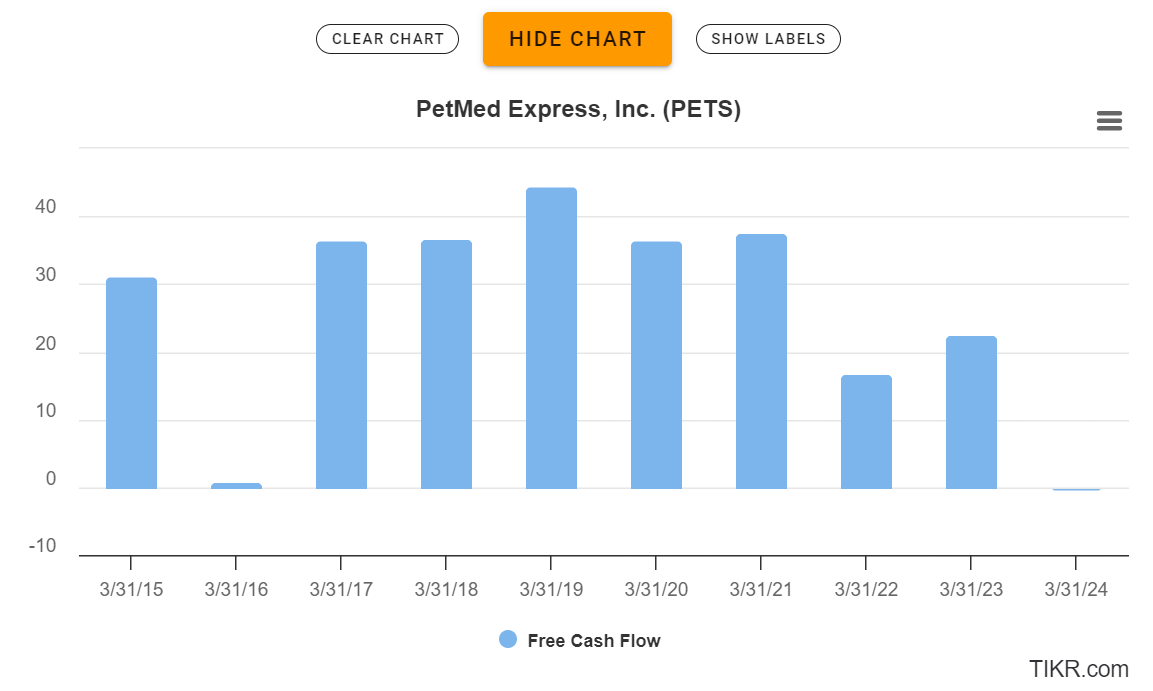

The business is highly cash generative and has minimal capex requirements. Even after the previous overspending of cash, the company still has $46 million in cash and no debt. Prior to the PetCareRX acquisition, maintenance capex ran around $0.5-$1.0 million per year. Even with slowing sales, free cash flow has remained healthy. The decrease in 2016 is for the purchase of the company’s property in Delray Beach, Florida.

In FY 2024, the company had to restate their financial statements due to incorrectly overvaluing their deferred tax asset by $5.9 million and understating their goodwill by $5.9 million from the acquisition of PetCareRX.

There are 20.5 million basic (20.9 diluted) shares outstanding as of June 30, 2024. The company has 2,500 shares of preferred stock outstanding and has 5.0 million in authorized preferred shares. The company issued 250,000 convertible preferred shares in 1998 and of the 250,000 only 2,500 remain. These shares convert into 4.05 shares of common stock. The net effect of the repurchase programs has kept the number of shares outstanding around in the range of 19-24 million since shares outstanding since 2004.

The most recent quarter was a somewhat mixed bag. Campos was only in place for two months during the quarter and is already working to stabilize the business. The top line comped negative, but the company earned a GAAP profit.

Market Opportunity and Competition

I personally don’t like TAM as a metric. However, in this case, it is safe to say the TAM is huge and has been continually expanding for the past 20 years. Pets continue to live longer resulting in more care for things like flea/tick/heartworm throughout their life and for more prescriptions as they age. I’ll leave any comments about TAM with this from PETS’s FY 2024 Annual Report:

“The total addressable market for pet medications, foods, and health products and services is vast and continuously expanding. According to the American Pet Products Association, pet spending in the United States increased by 7% to $147.0 billion in 2023, with veterinary care and prescription medications accounting for $38.3 billion or 26% of that total. The increasing demand for pet wellness products presents significant potential for us to expand our footprint and capture a larger share of this thriving market.”

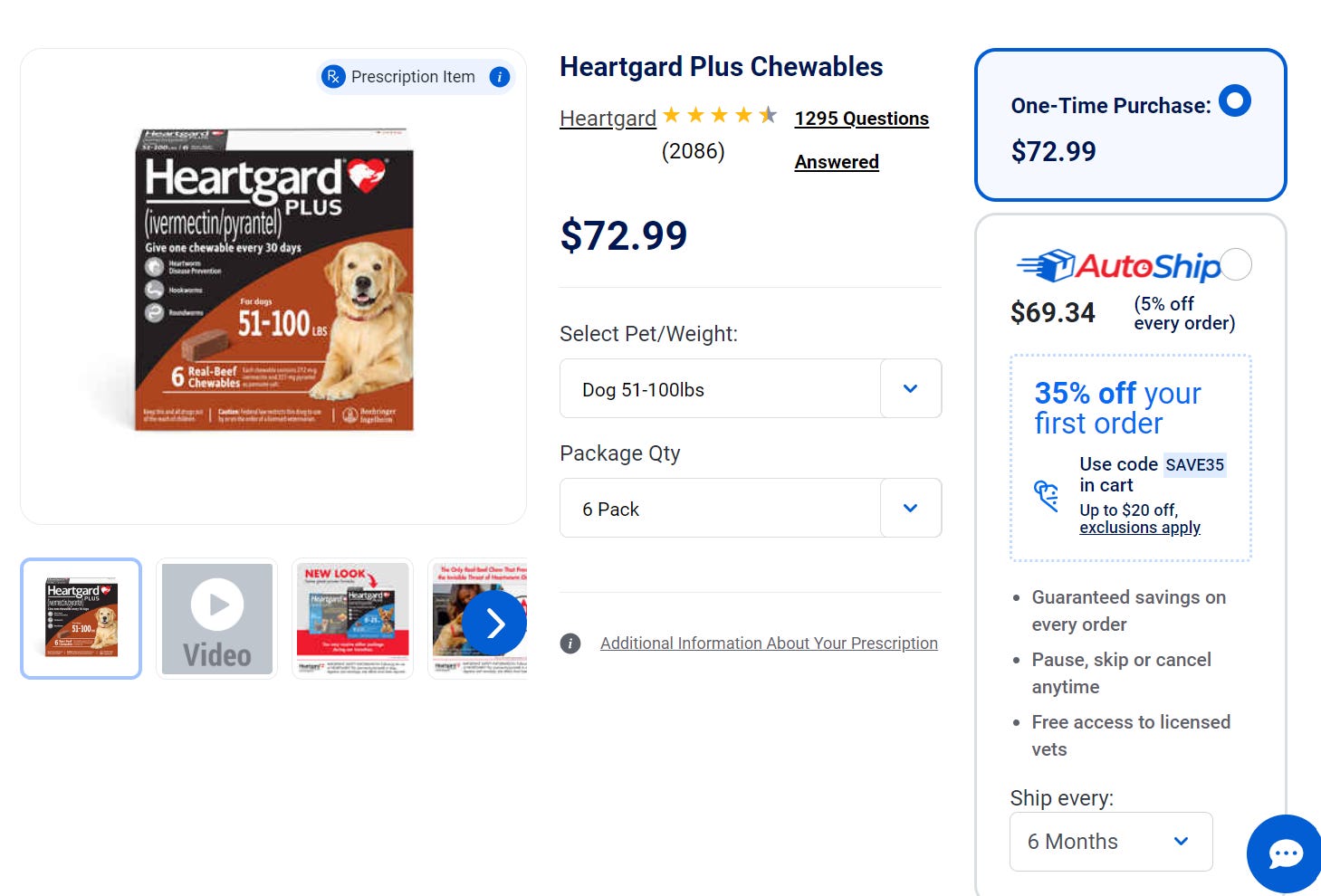

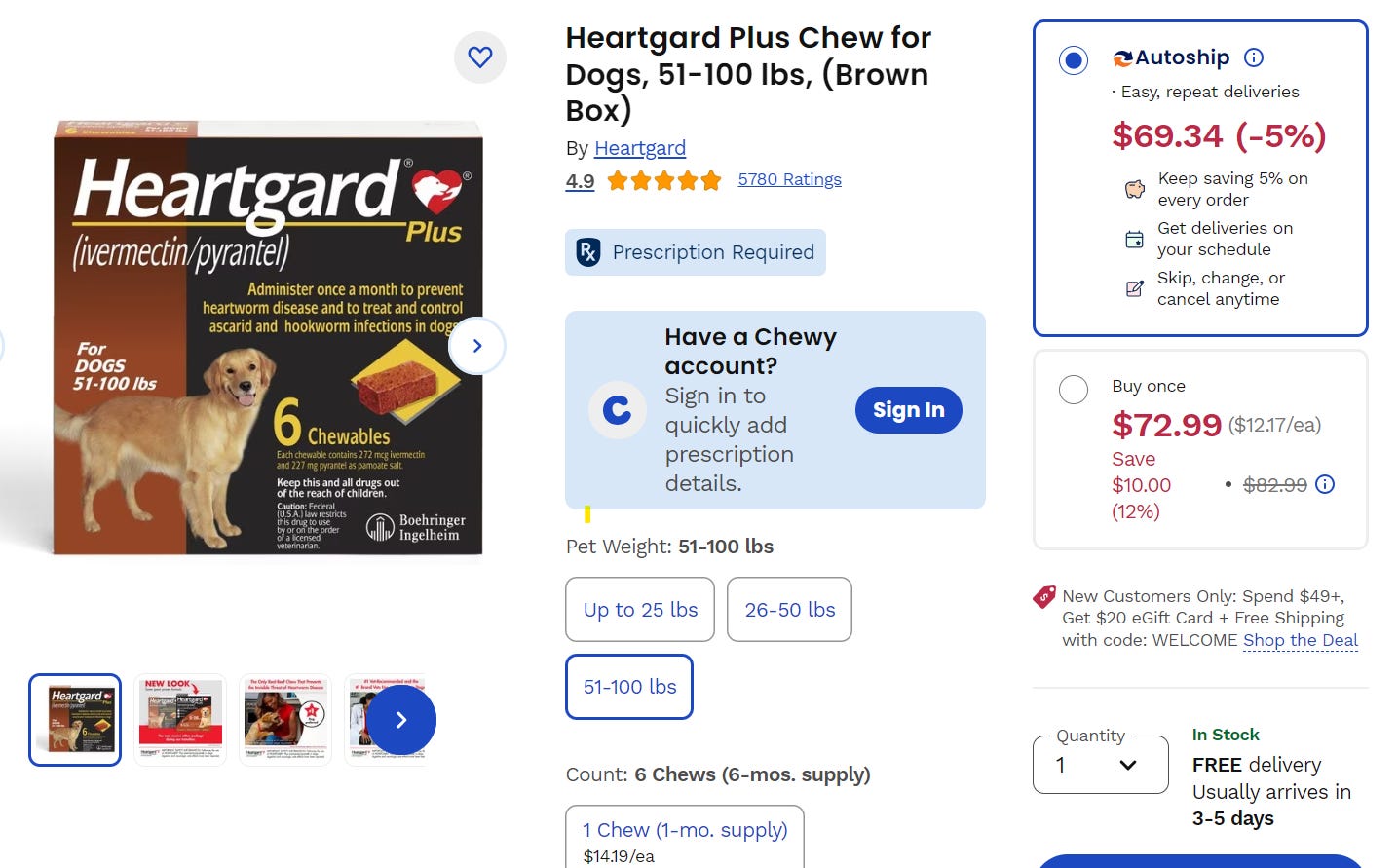

The industry is one of monopolistic competition with companies trying to differentiate themselves through service, product offerings, or loyalty programs. PETS adheres to minimum advertised pricing (MAP) pricing from their vendors and offers discounts when vendors allow them. The first picture is PetMed’s offering Heartgard Plus for dogs. The second picture is Chewy’s offering. Clearly, both companies cannot compete on price, so they will offer different discounts and rewards to attract and retain customers.

Why not Chewy, your local vet, or a low-cost pharmacy?

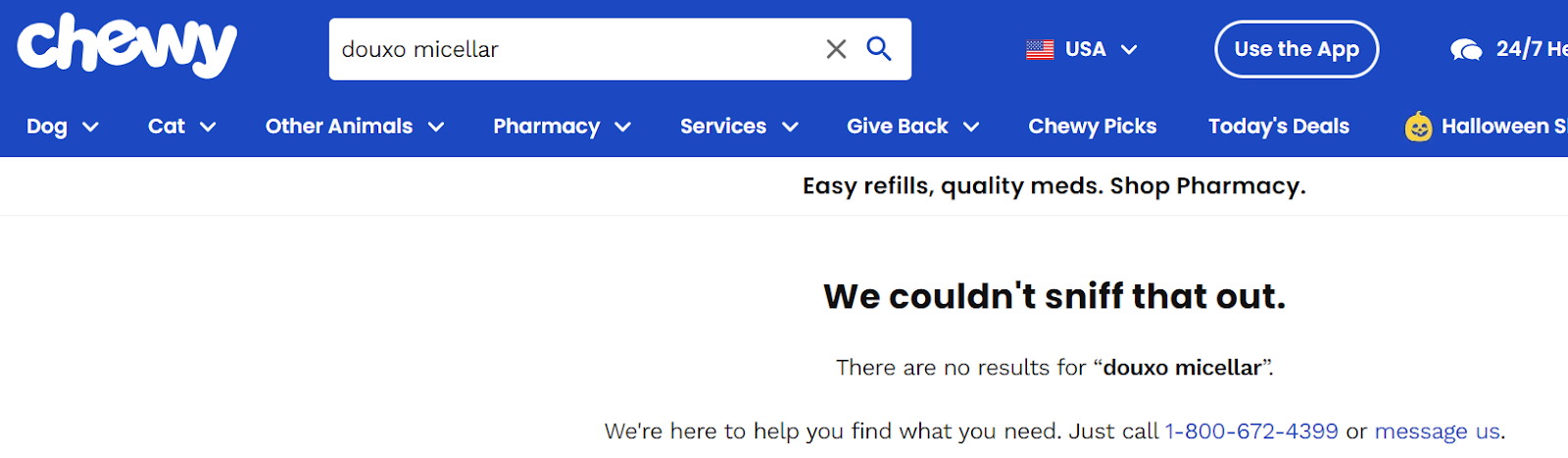

In two words, convenience and selection. My Catahoula loves finding swampy watering holes (even in the Midwest) and has a tendency to get ear infections from playing in water. Our local vet recommended an OTC ear cleaner called douxo micellar. Chewy didn’t have it in stock, PETS did.

There are alternatives in low-cost pharmacies like Costco. Although they are competitive on price, they are not as convenient as an online retailer that ships directly to your home and they are limited in their selection of prescriptions and OTC medicines. Lastly, local vets are convenient in the sense they are local, but they are limited by hours and not competitive on price.

PETS places themselves in the market as the most convenient, frictionless option. They have a strong autoship program and are working to make more products available on autoship. If you order a prescription from them, they will call your vet and work out getting the prescription for you. PETS understands customers are feeling economically pinched and work to have tiered pricing - offering 1-3-6 tablets at a time to give customers different price points. To be clear, the vet prescription convenience and tiered pricing has been copied by other competitors. This is a brutal retail environment where the only thing that is proprietary is a customer’s relationship with a company that is up for sale every day.

Management

Campos has wasted no time articulating a clear strategy and getting her own team in place. She has over 25 years of experience previously as CEO of Diane von Furstenberg and a host of apparel brands. Unlike Hulett, she is an avid animal person and has eight rescue horses, two rescue dogs, and a cat. She has been very clear that she is looking for individuals in her team that have experience scaling e-commerce brands.

Carla Dodds: Appointed as Chief Marketing Officer in May 2024. Dodds has over 15 years experience in marketing, strategy, and operations including Walmart and Mastercard.

Caroline Conegliano: Appointed as Chief Operating Officer in June 2024. Conegliano has nearly two decades of business experience with transformations in the consumer sector. The COO role was newly created specifically to focus on driving the company’s growth and profitability and enhancing customer satisfaction and service.

Umesh Sripad: Appointed as Chief Digital and Technology Officer in June 2024. Sripad has over 15 years of experience in technology. He served as the Chief Product Officer at PureRed, has been CDO at Bed Bath & Beyond, and CDO at IKEA, USA. He is focused on creating a seamless customer experience and enhancing online experiences for customers.

Doug Krulik: Appointed as Chief Accounting Officer in August 2024. Krulik has over 20 years of experience in finance and accounting.

Robyn D’Elia: Appointed as Chief Financial Officer in September 2024. D’Elia has over 25 years of experience in finance and accounting, including 24 years at Bed Bath & Beyond.

It is still too early to tell the impact all these new hires will make and CEOs bringing on their own team is nothing new. What is clear is that in aggregate these hires show a desire to focus on running the core business profitability, in a customer friendly way, and with good internal controls.

Insider ownership is low right now. The most recent proxy shows only 1.1% of shares are owned by insiders. However, that doesn’t account for the fact that there has been so much turnover in the company in the past 6 months. An author on Value Investors Club pointed out that Campos could be quite incentivized to sell the company based upon her employment agreement. She has 483,000 RSUs that vest over three years, but per her hiring agreement, a change in control that results in the company no longer being publicly traded would let her vest early.

The stock has always been fairly institutionally owned with BlackRock, Vanguard, and Renaissance Technologies LLC owning 8.4%, 5.57%, and 6.36% respectively.

I have not spoken to management yet - IR informed me they will reach back out after the company reports earnings in November.

Call Center & Board of Directors

I have not heard back from IR yet. I called 1-800-PETMEDS to buy the ear cleaner Chewy didn’t have in stock. I spoke to an employee who had been with the company for over 20 years. She informed me that Campos is holding town halls with employees to hear their concerns and perspectives on the company. She told me the feeling with her and her fellow colleagues in the call center roles was that she is finally turning the company around after the past few years.

One piece of valuable pushback I’ve already received on this thesis is that the Board of Directors is weak. I’d argue just like how it is too soon to judge management, it is too soon to judge the BOD.

The board that pushed out the CEO with a strong track record is not the board today. Only two members are the same. One of them, Gian Fulgoni, is 75 and stepped down as COB in January this year for succession planning - it’s not much of a leap to assume he’s on his way out.

The Board of Directors in 2021 - when they fired Akdag/hired Hulett:

Leslie Campbell

Peter Cobb

Gian Fulgoni (COB)

Ronald Korn

Jodi Watson

The Board of Directors today:

Leslie Campbell (COB)

Sandra Campos

Gian Fulgoni - stepped down from COB for succession planning.

Justin Mennen

Diana Purcel

Leah Solivan

Valuation

In the most recent quarter, PETS earned $0.18 in GAAP EPS. Annualizing this would give the company $0.72 in EPS which means the company could be trading around 5.5X NTM earnings. The company has traded between 12-38X earnings over the past 9 years, usually in the 12-22X range. Giving them a 12X multiple on $0.72 in EPS would put the stock at $8.64 or 117% upside from today’s price.

Another way to look at valuation through EBITDA multiples: In the 10 years before the old CEO, EBITDA margins were 10.1%-19.8%. Let’s say they can achieve 10% EBITDA margins on $270M revenue. The $270M revenue is slightly lower than the baseline revenue of the $280M or so they’ve been “stuck” in for the last few years and the PetCareRX acquisition was mismanaged. So, let’s say $27M EBITDA. Give them a 6X multiple - for being a small, fallen angel microcap in a competitive industry. That’s still $162M or once again, around 100% upside.

If the sale of the company rumors are true, there is a recent comp in the pet space. In August, PetIQ (PETQ) agreed to a buyout of $1.5 billion, or $31 per share in cash. This transaction was done around 15X TTM EBITDA for PETQ.

Risks and Mitigants

The online pet market is fiercely competitive. Mitigant: The company is re-focused on executing in their core pet pharmacy business.

This is a new management team and they might not execute. Mitigant: The company was GAAP profitable in the most recent quarter and has identified $5 million in annualized operating expense savings already.

The company had to restate financials recently. Mitigant: The company recently hired a Chief Accounting Officer.

Catalysts

Future profitability that will screen well and attract investors. At $0.18 quarterly EPS, annualizing, the company is going to screen around 5-6X earnings in the next year.

Resuming capital returns to shareholders.

Conclusion

This thesis doesn’t hinge on entering new markets or a rapidly growing business. For the company to be successful again and return to being highly profitable, they need to focus on their core pharmacy business and manage costs. The most recent quarter was an indication the company is doing just that. Although competition has increased, the stock could have a nice 100% upside or so in the next year if the company simply executes.

Disclosure: Long PETS.

For entertainment purposes only. This is not investment advice.

Thanks, Ninja. Have you had a look at their web traffic? On similarweb you can see for free their traffic between July and September. It went from 1.6mm to 1.1mm (number of visits). That trend is worrying, no?

So far, not a bad performance an great pick, but indeed still a lot of work for the CEO. Looking forward how it will perform in the future…!