KonaTel, Inc. (KTEL)

A countercyclical company ready to inflect in a difficult market environment

Introduction

The American Rescue Plan Act (ARPA), signed into law in 2021, pumped $1.9 trillion into the economy targeted to those hardest hit by the COVID-19 pandemic. One particular disparity brought into focus during the pandemic was nationwide broadband equity. Many individuals living in rural areas and lower-income zip codes lack a high speed broadband connection in their home. The inequity became magnified in a remote-first world: children fell behind in school, employees struggled to work remotely, and virtual doctor’s visits were completed at coffee shops and libraries.

The FCC’s recent Affordable Connectivity Program, launched December 31st 2021, has become a critical fixture to improve nationwide broadband access. This is where KonaTel enters as a way to ride the massive tailwinds of government funding and offer the potential for a nice return due its countercyclical business as inflation rages and American households look for a way to save money on their basic needs.

Konatel (KTEL)

Price: $1.43

Market Cap: $59 million

Shares: 41.6 million basic, 43.6 million diluted (no warrants or preferreds)

Insider ownership: 55.52%

Company Breakdown

KonaTel, Inc. (OTC: KTEL) is a national telecommunications carrier operating two subsidiaries. Apeiron is a Communications Platform as a Service (CPaaS) provider that supports business and consumer services. Infiniti Mobile is a FCC licensed Eligible Telecommunications Carrier (ETC) that distributes subsidized mobile voice/data services nationwide under the Federal Lifeline Program and Affordable Connectivity Program.

Apeiron

Apeiron Systems is a communications carrier that provides business and consumer services, primarily through their internally developed CPaaS platform. Aperion offers a host of services through their national network: voice, data, messaging, SD-WAN, etc. These services can be accessed through Apeiron’s APIs. Josh Ploude founded Apeiron in 2013, and has stayed on with Apeiron after KTEL acquired it for 7 million shares in 2018.

Other key CPaaS players like Twilio and Sangoma dominate Apeiron in terms of size and scale. Apeiron focuses on competing on price versus companies like Twilio and focuses on mobile (4G/5G/LTE) in its services. In 2021, Apeiron made the shift from an inbound only sales organization to an outbound sales organization. This pivot in focus has Apeiron poised for growth.

Infiniti Mobile

In January 2019, KTEL completed its purchase of Infiniti Mobile (d.b.a IM Telecom). As a licensed ETC, KTEL can offer a discount to low-income consumers on their mobile/voice service and receive reimbursement from the universal service fund administered by the Universal Service Administrative Company (USAC). Infiniti Mobile holds one of 12 active Lifeline licenses remaining today, and the FCC has not granted a new Lifeline license since 2012. Infiniti Mobile also collects subsidies under the Affordable Connectivity Program and previously under the Emergency Broadband Benefit Program. KTEL offers service on all three major networks (AT&T, Verizon, T-Mobile). Understanding the different subsidy programs and the amounts KTEL can claim takes some digging. Here is an overview of the subsidy programs:

Lifeline

The FCC established the Lifeline program in 1984 under the Reagan Administration to provide low-income households with access to low cost landline phone service. In 2005 under the Bush Administration, the FCC pushed to make Lifeline benefits available for wireless service plans. The Lifeline program is run by USAC, which is funded by telecom companies who pass this cost on to consumers, usually in the taxes & government fees section of their monthly phone bill. The subsidy for Lifeline is $9.25 per month for non-tribal land and $34.25 per month for tribal land. Lifeline participation is dismal, with most states reporting less than 30% of eligible households taking advantage of the subsidy.

KTEL is authorized to distribute Lifeline service in 9 states: California, Nevada, Oklahoma, Wisconsin, Kentucky, Georgia, South Carolina, Maryland, and Vermont. In their Q1 22 10-Q, KTEL hinted further state expansion is on the way:

“As part of the Company’s Mobile Service expansion plan, the Company took one-time legal and regulatory charges in the first quarter of approximately $103,000 to support expansion into additional Mobile Services distribution territories.” (emphasis added)

Lifeline differs from the ACP program in that ETCs must hold a Lifeline license and be approved by a state’s public utilities commission. A unique aspect of KTEL is they hold a federal lifeline license, which allows them to apply to enter any state nationwide.

EBB

The Emergency Broadband Benefit (EBB) program acted as a temporary subsidy established during the COVID-19 pandemic to help low income families with access to subsidized high speed mobile data connections. The EBB provided a $50 per month subsidy for non-tribal land and $75 monthly subsidy for tribal land. As of December 31st, 2021, the EBB was replaced by the ACP.

ACP

The $14.2 billion Affordable Connectivity Program (ACP) is intended to be a long term solution to the EBB program and provide high-speed wireless data to low-income Americans. ACP subsidies are $30 per month for non-tribal land and $75 per month for tribal land. Although there is marginal risk the ACP will run out in 4-5 years, even in a bitterly divided political climate, the need for broadband equity has been a consistent policy topic which receives bipartisan support. KTEL is authorized to distribute high-speed data under the ACP in the 48 contiguous states, Washington D.C., and Puerto Rico.

State Subsidies

Several state public utilities commissions offer their own Lifeline subsidy in addition to the federal subsidy. For example, in states KTEL provides Lifeline service, Wisconsin has a state subsidy of $9.25, Kentucky adds $3.50 per month, and Maryland has an additional $15 subsidy.

Average Subsidies

KTEL is able to claim both Lifeline and ACP. This means the average subsidies work out to $39.25/month for non-tribal land and $109.25/month for tribal land for states without their own subsidy.

Subsidies Concluded

KTEL has a structural advantage over other providers by possessing a federal Lifeline license. A large part of what has deterred other investors I have spoken with from this story is they believe there is an unpredictable risk of funding cuts to these subsidies. I wholeheartedly disagree. Lifeline has been around since the 1980s and survived under a myriad of different political makeups in D.C. Beyond that, Lifeline is funded by telecom companies who pass the cost onto consumers. The Lifeline program is nearly four decades old, operates outside the constraint of taxes, and helps low-income households; it is the ultimate win-win for politicians. The ACP program is funded for approximately 5 years based on disbursement amounts, and the overall benefits of connecting American households to high speed data outweigh the costs. Even if you want to take a dismal view that ACP will not be renewed, KTEL can still successfully scale and achieve the necessary growth for potential multibagger returns within the next 2-3 years.

Financials

KTEL reports under two segments, Hosted Services and Mobile Services.

Hosted Services

This segment covers Apeiron’s CPaaS solutions suite including services like VoIP services, SMS/MMS, mobile numbers, toll free numbers, SD-WAN, wireless data services, and SMS to Email. Hosted Services has grown nicely, but is still maturing.

In 2021, KTEL finished its final $800K amortization of Apeiron. With approximately 43 million shares outstanding, this immediately boosts EPS by ~$0.02 in 2022. Apeiron is growing, but the exciting part of KTEL’s story comes from the Mobile Services segment.

Mobile Services

The Mobile Services segment encompasses some of Apeiron’s business segment (carrier voice/text/data), but also includes subsidized mobile and data programs under Lifeline, ACP, and previously EBB.

With some approximation, it’s possible to figure out KTEL’s average subsidy from their Q1 press release and Mobile Services segment revenue from the Q1 22 10-Q.

"In order to effectively scale our business, we more than doubled our line count to approximately 23,000 lines over the past 90 days, the first significant increase in capacity in our history, with additional capacity to continue our growth.” - Sean McEwen, KTEL Q1 2022 Press Release (emphasis added)

Active Subscribers

Knowing KTEL had 23,000 subscribers as of March 2022, I estimated 11,000 and 17,000 subscribers for January and February 2022 respectively for 51,000 total lines of service during Q1. With $2.79 million in Mobile Services revenue, across the 51,000 active lines, this yields an average subsidy of $54.77/month. Management confirmed this is approximately right. As KTEL continues to grow and there are fewer tribal lands, it is realistic to assume the average subsidy per line will drift gradually down to $40-$45 per month when accounting for Lifeline + ACP of $39.25/month and KTEL targeting states with their own additional subsidy.

The rapid growth underway temporarily obfuscates KTEL’s true cost of providing subsidized service. KTEL fully recognizes customer acquisition costs at the time of activation which is temporarily depressing gross margins. Management doesn’t disclose the exact cost of service but has hinted it is in the high teens per line per month.

Looking at the average subsidies and cost of service is enough to understand why this business is growing exponentially and the inflection is already underway. The new influx of federal dollars made what was a nice targeted business (tribal) now a viable nationwide business. One caveat with the impressive subscriber numbers and growth is this is a business segment that experiences undisclosed churn due to consumers switching providers for new phones or not filling out the required annual paperwork.

Balance sheet

Management has taken advantage of the Lifeline and ACP opportunity, significantly tapping into financing to fund their growth.

May 18th 2022: Entered into a $3 million line of credit.

June 14th 2022: Entered into a note purchase agreement for $3.15 million at 15%.

In the Q1 2022 press release, KTEL disclosed:

"Furthermore, the additional $3 million in working capital will enable us to activate an additional 30,000 new lines of service each quarter. We can typically recoup customer acquisition costs in less than 120 days after activation, turning our cash resources at least three times every 12 months.” (emphasis added)

This yields insight into some dramatic possible scenarios. By adding 30,000 lines of service in a quarter and having it recouped in 4 months, there is a scenario where KTEL can easily add 90,000-150,000 lines of service over the next 12-18 months. Additionally, the debt raise could account for another 30,000 lines of service. Rationally, growing from 23,000 subscribers to nearly 200,000+ in 18 months is implausible, it is important to note management found a way to tap exponential growth in a way that minimally dilutes shareholders.

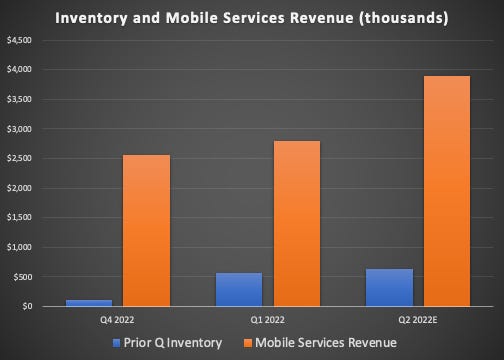

The company’s balance sheet leaves a clue about potential expansion through its inventory growth. When a customer signs up for Lifeline/ACP service, KTEL has to have a phone ready for them. Inventory has been a leading indicator for KTEL reporting large growth.

Management

As an investor, I’ve enjoyed seeing that McEwen methodically built and incentivized a highly qualified management team around him to capitalize on the opportunity. In 2022, Chuck Griffin, Jason Welch, and Todd Murcer all came into the fold with KonaTel.

Sean McEwen - Founded KTEL in 2014 as a Mobile Virtual Network Operator (MVNO). Prior to KTEL he served as executive management consultant to international MVNOs. Founded Online Data Corp in 1983 which eventually became TriTech solutions. TriTech evolved into an enterprise application and the first modern 911 dispatch system. Owns 17 million shares (~38%).

Chuck Griffin - President/COO KonaTel. Griffin has over 20 years of telecom experience and before joining KTEL as COO, Griffin served as Chairman of the Board and COO of Lingo Communications. Before Lingo he served as CEO of Impact Telecom. Griffin has experience building Impact Telecom from a startup company with four employees to over 400 employees and $250 million in annual revenue.

Jason Welch - President, IM Telecom. Prior to joining KonaTel, Welch served as COO at 46 Labs LLC, a SaaS, voice/data solutions provider for enterprise communications providers. Previously, Welch served as Executive Vice President of Impact Telecom, a Lingo Company, providing oversight to carrier wholesale sales acquisition, product strategy, account management, agent channel management, vendor management, pricing, routing and business analytics. He successfully managed the growth of the carrier wholesale business unit to $40m+ in annual revenues.

Todd Murcer - EVP Finance with two decades of telecom experience. Prior to KTEL, Murcer worked at Lingo/Impact Telecom as the Vice President of Financial Planning & Analysis. Murcer started at Matrix Telecom, where he helped the company grow from $10 million to $400 million in annual revenue.

Joshua Ploude - President, CEO, and Co-Founder of Apeiron Systems. Ploude has over 20 years of telecom experience and worked extensively with vendors to develop Apeiron’s product set. Prior to Apeiron, Ploude led the planning and construction of other national Competitive Local Exchange Carriers and Internet Service Providers. Ploude owns 6.3 million shares of KonaTel (~14%).

Brian Riffle - CFO. Riffle is a CPA with over 35 years experience and has been KTEL’s CFO since the company went public in 2017. Riffle has extensive financial experience in cloud computing and telecommunications.

Management has been fanatic about cost discipline. In 2021, KTEL’s best year to date, McEwen took a paltry $66,000 salary. In fact, when an investor raised a question about a percentage EBITDA provision in McEwen’s employment contract, he amended his contract to strike the clause (and he has never claimed it). Management has commented they are committed to predictable and consistent growth, both in revenue and net income.

One concern I had was the increase in the payroll and expenses line item on the income statement, which substantially increased, up 106% to $1.13 million in Q1 22 versus Q1 2021. When asked about it, McEwen said:

“G&A, for Infiniti Mobile (IM), will not increase substantially after this point because the primary leadership team is now in place. Future increases in payroll will include mostly lower-cost hourly folks in customer service and provisioning.”

I have two personal thoughts on management. The first is that McEwen had little trouble recruiting and incentivizing highly experienced telecom operators to join him at KTEL. This is valuable information in that others in the telecom world see how great the opportunity is to build and scale KTEL. The second is I have not come across too many CEOs like McEwen. There is no other way to sugarcoat it, he is obsessed with winning and building the business. In McEwen’s own words from our first exchange, “I love the fight (business is warfare to me).”

Valuation

Valuation scenarios with KTEL become ridiculous when assessing Infiniti Mobile’s growth trajectory.

Assumptions: KTEL ends 2023 with 130,000 lines of service, less than the 200,000 that is theoretically possible over the next 18 months. Average subsidies decrease to $45 from the mid $50 range currently. Cost of service per month is $19. OPEX doubles from ~$5 million to ~$10 million. Tax rate of 25%. Share count growth to 50 million from 41.6 million currently. 20-25 P/E for a business with high recurring revenues and guaranteed funding for the government. This could put the stock in the $9-11 range by the end of 2024.

(((130,000*12)*($45-$19) - $10,000,000) * .75) / 50,000,000 = $0.46 EPS

20 P/E: $9.17/share

25 P/E: $11.46/share

Many might find that growth trajectory unrealistic. As a sanity check, let’s assume KTEL tops out at 30,000 subscribers and stops growing for the rest of the year. The next 9 months at 30,000 subscribers at the average $54.77 would yield $14.58 million in revenue for a total 2022 Mobile Services yearly revenue of $17.37 when adding in Q1 numbers. Including zero growth in Hosted Services would be approximately $22 million in revenue for 2022. For context, KTEL ended 2021 with a total of $12.8 million in revenue. I view this as proof in real time that KTEL’s exponential growth is already underway.

Risks/Caveats

Funding - Despite it being improbable, there is the outside chance the ACP runs out and is not renewed. Even if that is the case, the ACP is funded for 5 years and KTEL’s growth can happen within the next 2-3, before concerns about funding cause multiple compression.

Churn - Lifeline churn is a risk. The churn can come from customers switching providers to receive a new phone, wanting to jump networks, or not updating their required annual paperwork to stay eligible. KTEL has several levers available to them, like offering new phones and the fact they provide service on all three major networks.

Share Structure - The main risk I view right now is making sure KTEL does not significantly bloat its share structure or incur too much debt while managing their growth. Management has made it clear they are focused on profitable growth though and beyond that, the insider ownership provides a reasonable cushion against non-accretive actions.

Conclusion

With the ACP program underway, state expansion, and a highly qualified management team, KTEL is inflecting into massive growth. Beyond that, KTEL has a natural moat by holding a federal Lifeline license which gives them high subsidies relative to ACP-only providers. In my personal view, KTEL is one of the rare opportunities that comes up once every few years that can change the trajectory of your portfolio.

Are you still long this thing? End of 2023 is approaching fast and we‘re nowhere near KTEL being a profitable company trading at 20x P/E. What went wrong? Are you still hopeful?

Any help to tracking the subscriber's amount? I made QoQ growth / 3 months / ACP aid to get uit