Cornerstone Financial plc (CSFS.L)

Transformation behind them, profits ahead.

Price - 13p

Shares Outstanding - 55,791,324

Market Cap - £7.3M

Enterprise Value - £8.6

Executive Summary

Cornerstone FS plc (AIM: CSFS.L) is a business that has undergone significant transformation not yet apparent in their numbers. The business previously operated as an unprofitable, low-margin white-label payments solution. Under new CEO, James Hickman, the company has:

Scaled down most of their low margin white label customers.

Shifted focus to higher value private clients instead of being a B2B currency exchange.

Sold off acquisitions to non-competing companies while keeping their primary financial license.

Refreshed its board.

Business Overview

Cornerstone FS plc is a fintech company focused on foreign exchange and payment solutions for businesses and high net worth individuals (HNWI) with offices in London and Dubai. Through their Financial Conduct Authority (FCA) license, Cornerstone is an authorized Electronic Money Institution. In English, this license allows Cornerstone to operate International Bank Account Numbers (IBAN) for their customers. This is different from other solutions like international SWIFT wire transfers from US banks to international accounts or doing one time payments through a traditional payments platform like PayPal. Despite being a simple spread-based currency exchange business, Cornerstone is gaining traction in the space. A key differentiator is a low-tech solution for the high tech payments industry: the telephone. Cornerstone is gaining and retaining HNWI clients through conducting most of their transactions over the phone to assure their clients they are getting great service and favorable conversion rates on their money. Most HNWIs are people doing large transactions such as people living in Asia and purchasing a second home in the UK, not doing small remittance transfers to family.

Financials

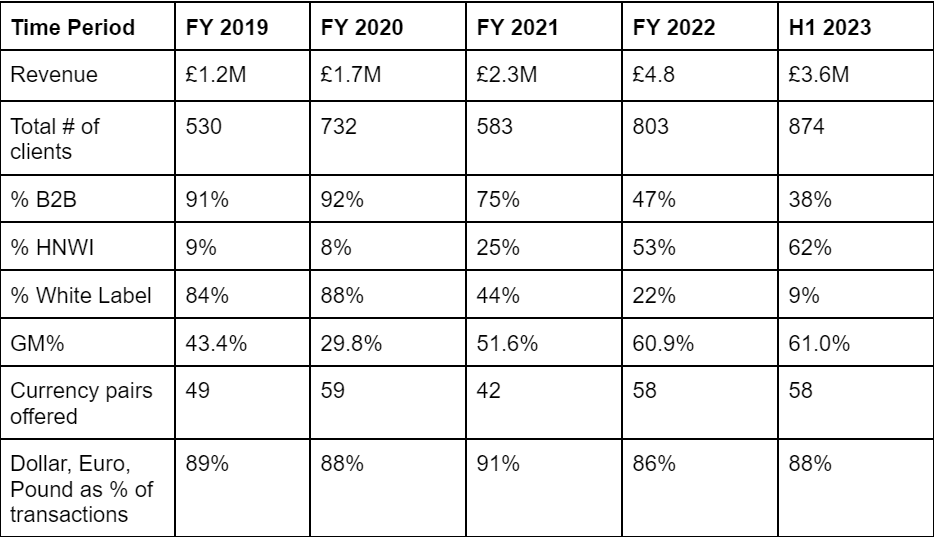

The financial profile of Cornerstone could best be summed up in the table that looks at key metrics. H1 23 was the company’s best ever half, which included a heavily adjusted EBITDA profit (sale on subsidiary disposal, interest on client’s money). Even with that, I believe the company is going to emerge with a strong financial profile that doesn’t screen well, yet.

From 2019 to 2022 revenue grew from £1.2M to £4.8M, around a 58% CAGR. This growth was facilitated by a few factors. Namely, Cornerstone increased its transactions to HNWI and decreased B2B transactions. Additionally, the company shed most of its white label revenue, bringing gross margins to around 61%, where they are projected to remain.

In H1 23, the company posted record results. Revenue was £3.6M (up 90% from H1 22) with 61% gross margins. Adjusted EBITDA £190K was and CFFO was £113K. Total opex for the business in H1 23 was £2.24M against a gross profit of £2.2M. The company’s first operating profit came from a line in their income statement called “other operating income” which is the interest Cornerstone accrues from their client’s cash balances. This led the business to a £138K operating profit for the half, or .06p earnings per share. From their H1 23 Investor Meet Company call, management had three extremely bullish remarks. First, management reiterated several times they expect FY 23 to be significantly ahead of market expectations. Second, management discussed that they are continuing to develop and enhance products and anticipate announcing a decision on a new payment card program in the next few weeks. Third, Shore Capital picked up Cornerstone FS and is beginning to cover the company.

Cornerstone’s balance sheet has £816K in cash against £2.2M in debt. £2M of this debt is owed to Robert O’Brien and his Dubai-based team as part of their compensation structure. This debt is held on friendly terms and has already been amended once to extend the payment term out a year to help the company use its cash for growth. The company has around £5M in NOLs and does not anticipate paying income tax in the medium term.

Company History and Timeline

Cornerstone was founded in 2010 under the name PlutusFX LTD as a way to more efficiently serve the B2B market for foreign exchange transactions. By 2016, Cornerstone began white labeling their FX solution to other FX companies. Cornerstone’s brief history as a public company is best divided into two periods - one with Julian Wheatland as CEO and the new era with current CEO James Hickman.

The Wheatland Era

In April 2021, Cornerstone went public on the AIM exchange, raising £2.69M via 3.6M shares at 61p and a £450,000 convertible loan. At the time, Cornerstone had 26 white label partners and was just starting to serve HNWIs. Cornerstone was led by former CEO Julian Wheatland. If the name sounds familiar, that is because Wheatland was an executive at Cambridge Analytica during their Facebook data scandal. Like Cambridge Analytica, Wheatland’s involvement in Cornerstone was messy. Under Wheatland, the business acquired three businesses:

FXPress Payment Services (September 2020) - Advanced payment systems to serve as a platform as a service to SMEs. FXPress became the Group’s main operating entity when Cornerstone disposed of their consumer business and adopted the name Cornerstone FS plc.

Avila House Limited (October 2020) - Licensed small e-money institution focused on multi-currency e-wallets. Acquired for £60,000 in shares and £32,685 in cash.

Capital Currencies Limited (January 2022) - Raised £0.85M through shares at 26.5p with a total consideration of £3M through cash, shares, and convertible notes. Capital Currencies Limited is a foreign exchange broker focused on currency exchange and international payments.

In 2021, FXPress Payments Services Ltd was approved by the Financial Conduct Authority (FCA) to be an Authorized Electronic Money Institution. This allowed Cornerstone to broaden their product offering by acting as a participant in the UK’s Open Banking Initiative. This lets customers leave money in their account - giving them a multi-currency account and e-wallet functionality. This is a key differentiator for the business - many payment services do not have IBAN capabilities to retain money in your account. For businesses doing frequent international transactions or HNWIs, this solves the need for slow, recurring wire transfers.

Additionally in 2021, Cornerstone established an Asia team to expand their focus on HNWIs. To accomplish this, Cornerstone recruited the team from their top white label partner, Vorto Trading Ltd. to lead the Dubai-based Asia team. Under the leadership of Robert O’Brien, this office has become the key growth driver for the company, demonstrated by the % increase in HNWI as a percentage of revenue and overall growth in the business.

The Hickman Era

In July 2022, the company announced Julian Wheatland was stepping down. The new CEO, James Hickman, was announced in August and started his role in September 2022. This proved to be a turning point in the business. The Wheatland era was marked by low margins, dilution, and apparent duplicative acquisitions. I’d argue the Hickman era is marked by stabilizing margins, managing the business for profit/cash, and laser focus on avoiding dilution.

In September 2022, Cornerstone acquired Pangea FX Limited for £200,000 (£25K cash, £175K loan). Pangea FX is a specialist FX and treasury consultancy focused on helping corporate clients control the impact currency volatility has on their business. The real driver behind this acquisition was the sales team Cornerstone acquired, Joe Jones and Stuart Plummer. Jones and Plummer founded the business and both previously worked at Vorto Trading as senior sales executives. The team is split with Jones based in London and Plummer in Dubai. In the same month, Cornerstone announced a partnership with Singapore-based Atlantic Partners Asia to provide currency and payment solutions to HNWI.

In December 2022, Cornerstone announced it was selling Avila House to non-competitor Aspire Commerce. The sale was completed in April 2023 for £300K in cash plus a licensing agreement that guarantees Cornerstone a 12-month minimum of £290,000 in revenue. This was a coup for a business that had £197K revenue and £2.4K profit in FY 2021. September 2023, Cornerstone completed a similar sale, disposing of Capital Currencies for £150,000 in cash. Both of these disposals provided Cornerstone with cash for operations and shed their more limited FCA licenses than the one Cornerstone already uses through FXPress.

Management/Key Employee

James Hickman

Much of this transformation underway is owed to the new CEO James Hickman. Hickman has an impressive background with over 20 years of experience in the FX and payments industries. Prior to joining Cornerstone, Hickman was CRO at Fire Financial Limited Services, spent time at AIM-listed Equals Group plc, and Caxton Payments Limited. In all his previous roles, Hickman has been responsible for growing sales and efficiently managing operations. In my interactions with Hickman, I’ve found him to be forthright and extremely focused on controlling costs while innovating new products.

In asking about what he learned from Equals Group that he brought to his role at Cornerstone, he informed me that he was brought on specifically to increase the B2B side of the business through organic growth and inorganic growth. He learned the value of having a broad product spread and customer base spread and is now in the beginning phases of replicating at Cornerstone. Importantly, Hickman mentioned he is trying to do this through partnerships rather than internally to control costs.

When asked about the strategic direction for the business over the next few years, he said:

“Our strategic focus is very much increasing our product capability and regulatory footprint. Ultimately being able to serve more customers globally with different payment methods. Including bank to bank, cards and more. This very much includes increased payment capabilities. We are now on a firm footing and whilst our focus is remaining cash generative we will be investing when there is a clear ROI.”

Robert O’Brien

Robert O’Brien is Cornerstone’s General Manager for APAC and the Middle East. O’Brien has 15 years of FX experience and joined Cornerstone from Vorto Trading Ltd. At Vorto, he was the largest revenue generator and built the business based on transactions from Asian clients investing into the UK. O’Brien and his team joined Cornerstone pending a significant compensation agreement. Under the agreement, O’Brien was entitled to receive share-based compensation related to a multiple of his revenue generation and contribution towards profit during the first two years. Fortunately, and unfortunately, his Dubai-based team performed exceedingly well. When Wheatland left the business, O’Brien’s expanded responsibilities left him entitled to £2,940,000 paid out over 3 years. After a couple iterations, this ended with O’Brien agreeing to the aforementioned £2M note at 6% and shares. After an issuance in February 2023, O’Brien owns 9.4 million shares (16.4%). Hickman said he has an excellent working relationship with O’Brien and both are aligned on the direction of the business. He said that O’Brien is just as focused on growing the business with both reputation in the space and shareholder value. Importantly, in the H1 23 call, the company said there are no more payments to O’Brien and the dilution/debt for compensation is over.

The Board

Lastly, in 2022, there was massive turnover in management and the board. Former CEO Wheatland stepped down. Directors Stephen Flynn, Glyn Barker, Elliott Mannis, Phil Barry, and Daniel Mackinnon all stepped down. This is obviously a red flag, so I point blank asked James Hickman about this. His response:

“You are right in that there has been significant change both at PLC board level and executive level. However, this was absolutely necessary to put us in a position where we can scale the business and really start to make an impact. Payments is a complicated beast and any business involved in this space needs the expertise across compliance, operations and finance to be able to run a successful business. I am now very happy with the team we have in place and don’t expect any changes in the near future.”

Competitors

Cornerstone is a small player in a competitive space. Public comps like Agrentex Group plc (AGFX.L), Alpha Group International plc (ALPH.L), and Equals Group plc (EQLS.L) are much larger. These companies tend to focus and innovate on B2B transactions, while Cornerstone is clearly focused on product innovation and expanding reach to HNWIs.

Interestingly, when discussing competitors with the company, Hickman mentioned three completely different (private) companies that he respected and thought were well run: WorldFirst, which has grown rapidly and is now owned by ANT Financial Group; Ebury, which was acquired by Santander for £350M in 2019; and Caxton, who has been first to the market with different innovative products. Hickman pointed out that the similarity in all three of these businesses is that they are diversified across different products and customer bases.

Risks

Key person risk - the largest shareholder and sales driver is Robert O’Brien.

Competition - this is a competitive space with an absurdly simple business model.

Execution risk - it remains to be seen if the company can expand into new products and customer bases while staying profitable.

Valuation

Doing some back of the envelope math, I could see a reasonable argument that this business is trading at <10X operating income over the next 6 months as FY 23 results are announced. First, the company announced it is trading significantly ahead of market expectations and has hinted they will be delivering a new product to the market. Assuming H2 revenue grows 15% sequentially, the business will end up with ~£7.6M of revenue for the year. At 61% gross margin, gross profit will be £4.6M. Annualizing H1 opex gives £4.5M in opex and doubling the other income (interest on cash), giving the business just under £500K in operating income for the year, or 1.5p on a 14.25p stock vs. (admittedly larger) competitors who trade on EV/Revenue and EV/EBITDA multiples.

Conclusion

Cornerstone FS plc is a significantly improved business over the past year that has a lot of surface level red flags - shady former management, related party notes, excessive board turnover. Once you dig past the red flags, this is a unique, growing business led by a competent, innovative management team, on the cusp of sustainable profitability, with dilution in the rear view mirror.

Disclosure: Long a small position.

This is an excellent writeup. Just curious, how did you find this stock?

Were you reading all of its financial updates/filings whenever they published an interim update back in 2022? Thanks!