Coral Products plc (CRU.L)

An under the radar quality microcap.

Price: 14p

Market Cap: £11.67M

EV: £6.6M

Shares Outstanding: 83,402,589

TTM Diluted EPS: 1.17p

Insider ownership: 20.9%

Dividend Yield: 7.5%

Executive Summary

Coral Products is an AIM-listed speciality plastics manufacturer based in Manchester, UK. Recently, they have sold off their two high-volume plastics subsidiaries, their experienced CEO left, and the company sold off its building and land from these subsidiaries that provided them with £300,000 in annual rental income. Now, their 75 year old Executive Chairman, Joe Grimmond is left to run the business. So who would be interested in this?

What if I told you Grimmond describes the business as a “profitable, well-managed, cash generative, dividend paying, cash-rich business, operating in niche markets forecast[ed] to grow over next 5 years.” From my early due diligence, it appears that every word of that statement is true.

Company History and Timeline

Coral Products plc was founded in 1989, listed on the LSE in 1995, and moved to the AIM Exchange in 2011. Over the past decade, CRU.L has made several strategic moves in building out their niche in specialized plastics manufacturing. Here are the relevant ones to the investment case:

2012: Acquired the land and buildings for their Haydock (manufacturing) facility

2014: Acquired Tatra Plastics Manufacturing Limited for £2.0M cash and £0.5M in shares.

2016: Acquired Rotalac Plastics Limited out of administration for £160,000. Acquired Global One-Pak Holdings for £2.95M cash and £0.65M in shares. Merged Tatra and Rotalac into Tatra Rotalac.

2021: Disposed of Coral Products (Mouldings) and Interpack Limited for £9.4 million to One51 ES Plastics Ltd. Repaid mortgage on Haydock facility for £1.5 million. Acquired Customized Packaging Limited (CPL) for £1.25 million, £883,000 cash, £366,000 in shares. Repaid £1.6 million mortgage on Haydock facility, paid off their CBIL loan, leaving the company debt free.

2022: Acquired Film & Foil Solutions Limited for £3 million, £1.348 million cash, the rest in a split between shares and an escrow account. Acquired Alma Products for £1.5 million in cash. Acquired Manplas for £300,000 (£200,000 cash, £100,000 shares above market price).

The Dreaded Haydock Facility

From the time the company bought it in 2012 to its disposal, Coral had a tale of two businesses. Haydock housed Coral Products (Mouldings) and Interpack Limited. These two subsidiaries were high volume plastics manufacturers that competed with global conglomerates. Coral Products (Mouldings), through plastic injection molding and extrusion, makes things like plastic stackable containers and rectangular recycling bins. Interpack Limited, which permanently moved to the Haydock facility in 2015, is an injection molding producer of food containers, recycling bins, buckets, etc.

Coral’s Haydock facility ended up causing a lot more headaches than it solved. In the words of Grimmond, Coral was “too small to be large and too large to be small.” Through three CEOs plus Grimmond as Executive Chairman several times, the Haydock facility could never produce consistent results or profitability. The company was aware as early as 2014 when they commissioned an independent review of operations to make improvements. Despite the commitment to improve the facility, these two subsidiaries and this facility consistently burdened Coral’s results and negatively impacted margins, masking the strong progress Coral was making in their niche plastics subsidiaries.

As part of the sale agreement to One51 ES Plastics, CEO Mick Wood left to join the acquirer. After some roof repairs, Coral sold off the Haydock facility and this sale along with the subsidiaries sale left Coral with over £7 million in cash, debt free, and holding two profitable, niche subsidiaries that accounted for only 25% of the sales but carried better gross margins. Here is what Grimmond told me about making Coral’s moves and the benefits in disposing of the Haydock facility:

“The cash eliminated our debt and produced a substantial surplus. Our other profitable operations could then take advantage of this debt free situation to invest for organic growth. By developing new products and improving production capacity. More time at board level concentrating on earnings enhancing activities rather than fire fighting.”

Business Overview

Through its six fully-owned subsidiaries, Coral manufactures and distributes plastic injection, extruded, and vacuum formed molded products into diverse range of sectors including manufacturing, health services, telecommunications, railway, automotive, and retail. Moving forward, Coral’s strategy is focusing on niche products for their 500+ customers that are small to medium volume rather than the 100,000 per week volume of plastic boxes/containers. The subsidiaries are:

Tatra Rotalac Limited - Manufacturer of plastic injection moldings and extrusions

Global One-Pak - Design, packaging, and distribution of lotion pumps, trigger sprays, and aerosol caps

Customised Packaging Limited - Manufacturer of plastic injection moldings and extrusions

Alma Products Limited - Extrusion, thermoforming, and container printing (acquired May 2022). For 2021, Alma is forecasting sales of £12.3 million and profit before tax of £264,000.

Film & Foil - Flexible packaging films, print lamination films, speciality plastics, paper, and aluminum foils (acquired May 2022). Per unaudited 2020 financials, Film & Foil had revenue of £10.1 million.

Manplas Limited - Vacuum formed products (acquired September 2022). For 2021, Manplas’ sales were £2.7 million with a loss after tax of £29,000.

It is intentional that there is a lot of overlap between subsidiaries, which plays into Coral’s growth plans moving forward - continue growing organically while making earnings accretive acquisitions when available. For reporting purposes, these segments are broken down into extrusion, spray and nozzles, and vacuum formed products.

Right now it is unknown if Coral plans to break out into another reporting segment like films & containers after its three recent acquisitions. Under Coral’s new niche strategy, the company has grown rapidly, with a temporary decrease in trigger sprays & nozzles caused by China supply chain issues that are anticipated to resolve over the next year.

One differentiating aspect of Coral in the small UK plastics sector is their extensive use of recycled materials. Starting in 2019, Coral launched a 360 degree recycling facility. Customers buy products from a subsidiary, use them, and return the used product when they are done. In turn, they receive money back and Coral has material they can re-use as a sustainable plastics business. This recycling facility was located at their Haydock facility and made Coral an attractive sale to One51. Despite the sale, Coral’s subsidiaries still have these recycling capabilities available for customers.

Financials

Over the past decade, Coral has focused obsessively on shedding declining customers/industries, growing margins, and maintaining profitable operations. Unsurprisingly, their main input cost is materials, which average around 40% of their costs of producing a product. Coral maintains a wide group of suppliers and importantly, is able to pass on their increased costs to their customers. In the chairman letter, Grimmond mentioned Coral Products plc has their energy prices locked in for the year, pre European energy crisis, and does not expect any impact on energy costs for the year because of this.

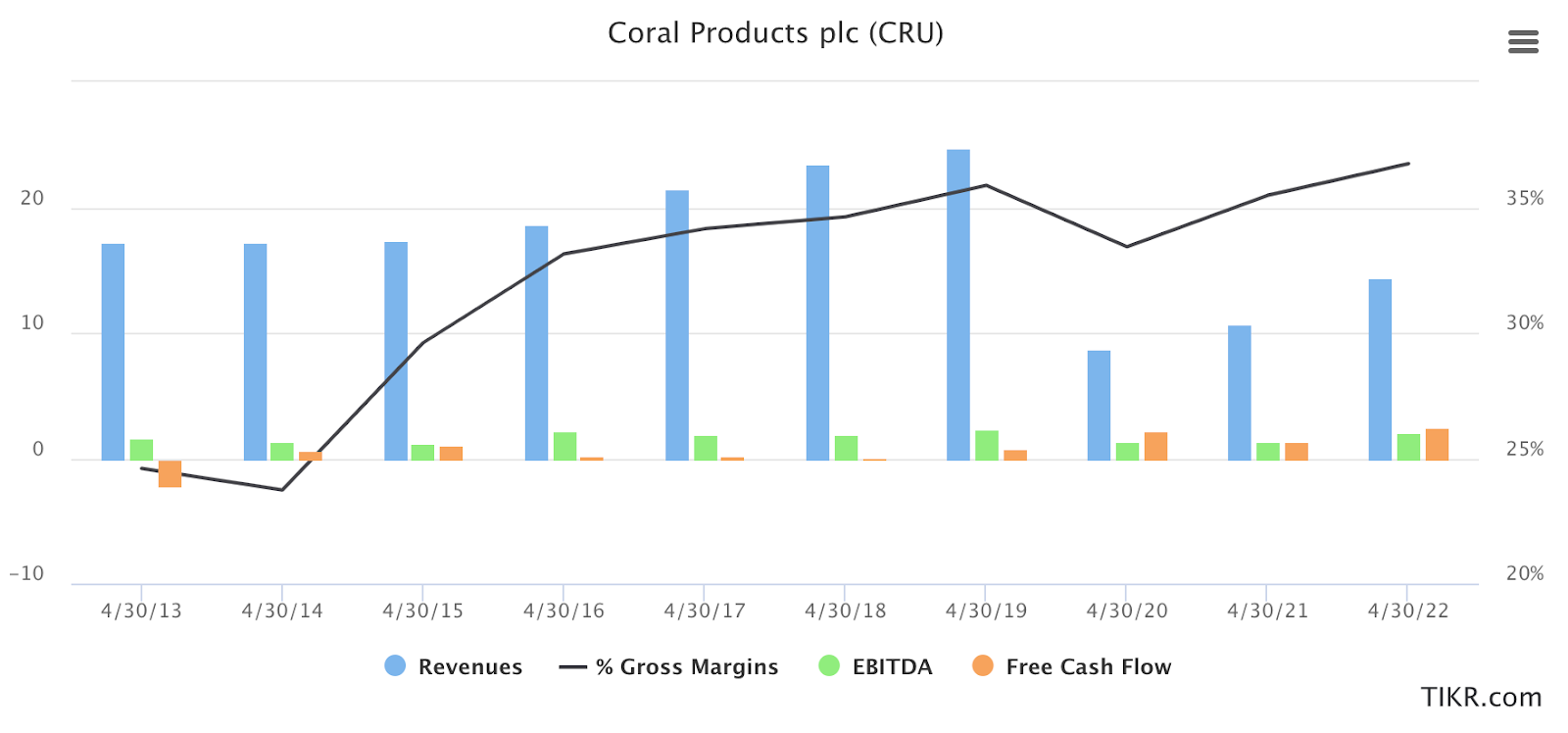

The chart below shows the impact of Coral’s strategic direction over the past decade. First, Coral sold off their high volume on leaving the CD/DVD casing business in the early 2010s which had low margins and customer payment issues. Leaving these customers and eventually selling these businesses off halved revenues but have shown consistent improvements in gross margins. Second, Coral has been able to significantly grow their EBITDA margin and free cash flow with their new niche strategy. Presently, CRU.L trades for less than 4X EV/EBITDA and less than 5X free cash flow per share.

Coral has a strong balance sheet with £7M cash and the only liabilities being an invoice facility secured against their receivables and leases. With the exception of 2020, CRU.L has consistently paid dividends from 2012-2022, however the payout ratio has routinely gone over 100%. This has been masked with a healthy balance sheet and should be covered by net income growth, but is something to note.

Although shares outstanding grew over the past decade, this stopped in 2016 after the acquisition of Global One-Pak. Since then, shares outstanding have stayed ~80 million and no stock options were exercised in 2021/2022. The company has made effective use of their buybacks, choosing to hold these shares in treasury to then re-issue again for acquisitions (usually a 66/33 split of cash and equity). In 2021 and 2022, the company repurchased 8.5% of shares outstanding and held them in treasury, using them for the CPL, Film & Foil, and Manplas acquisitions.

Management

Joe Grimmond has been with Coral since 2011 and has been the classic microcap executive chairman investors want: he owns 7.9% of the shares and routinely buys more, doesn’t take an excessive salary, and has personally loaned the company money previously to bridge a working capital funding gap (nearly a decade ago from declining CD/DVD operations). He’s a no nonsense operator with 30 years experience in the plastics industry. When I spoke with him reflecting on how he has learned from past experiences, he provided a master class every investor should look for when evaluating management:

“What I have learned is watch the cash, clear divisions of responsibility and accountability. Prompt reporting of actual performance against budget. Prepare to flex budgets up or down if conditions change. Act early; admit / accept mistakes then act to correct or mitigate. Don't let customers run your business. Customer is King but only if he pays the price.Otherwise he is Master.”

Coral’s focus on sustainable plastics and recycling is not an accident, as Grimmond maintains certainty that plastic that cannot be broken down will one day be taxed out of existence. Management is working to position the company for the future now so they are not caught off guard as plastics become more expensive to manufacture.

Paul Freud serves as the Corporate Development Director with over 20 years plastics experience. Freud is responsible for business development opportunities and seeking out acquisition candidates, including the three completed this year.

Philip Allen was appointed as Coral Products plc’s Group Operations Director in April this year and has over 35 years plastics experience. Before joining Coral, Allen worked at Tatra in 2011 and served as the managing director of Tatra Rotalac in 2018 and CPL in 2022.

The Board collectively has over 100 years experience in the plastics sector and insiders own 20.9% of the company. Historically when a company has been bought out and brought in as a subsidiary of the group, the management has stayed to continue running the business.

Competitors & Valuation

Coral has two direct competitors that are listed in the UK, Robinson plc (RBN.L) and Carclo plc (CAR.L). A key difference between Coral and their competitors is their balance sheet. Coral has a strong net cash balance while RBN.L has net debt of £12.2M and CAR.L has net debt £32.4M. Adding in the sales of Alma, Film & Foil, and Manplas, all of which were acquired this year without taking on any debt, could yield an additional £10-13 million of revenue in the next 12 months while Coral continues to seek out accretive acquisitions to pair with their organic growth. WH Ireland previously covered the stock and valued them at 4.6X EV/EBITDA. Cenkos Securities plc currently covers the stock with a 20.8p price target. . However you want to value it, CRU.L is cheap: 3.7X EV/EBITDA, 4.6X FCF/share, 11.7 P/E.

Risks

Possibility of bad, non accretive acquisitions

Rising materials costs/energy prices

Dividend payout ratio

Conclusion

CRU.L is a high quality, niche plastics producer that trades for less than 5X free cash flow/4X EV/EBITDA run by experienced operators with significant insider ownership.

I think you are definitely onto something, despite there being no improvement in price sine you posted this. The aquistions appear on paper to be fantastic. Usually below net assest value and low earnings multiples.

The management are clearly aligned.

I think this is a turn around story and your analysis will be correct.

Fantastic write up! You never disappoint in your ability to expose undervalued gems! What brokerage account did you use to buy CRU?

I recently opened a Fidelity account to purchase some international stocks... but, it doesn't allow trading on CRU, even though it allows trades on other AIM equities.